Thursday last, I was somewhat shocked to receive the following missive from one of my brokers, TD Direct (now owned by Interactive Investor):

The key paragraph is this:

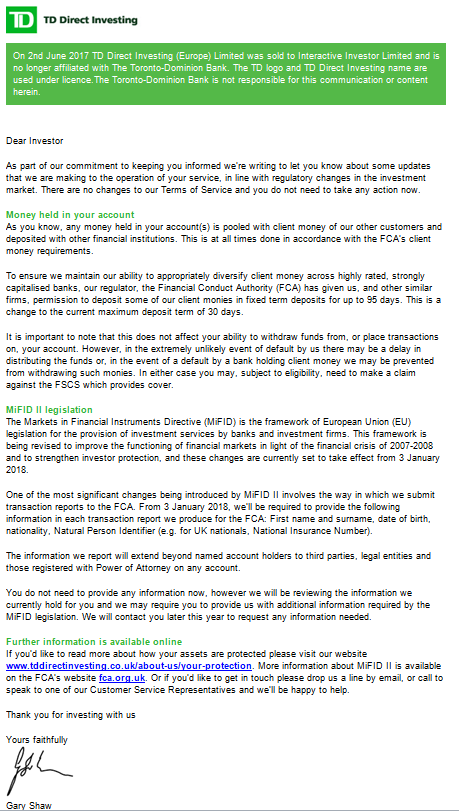

To ensure we maintain our ability to appropriately diversify client money across highly rated, strongly capitalised banks, our regulator, the Financial Conduct Authority (FCA) has given us, and other similar firms, permission to deposit some of our client monies in fixed term deposits for up to 95 days. This is a change to the current maximum deposit term of 30 days.

ISTM that there is zero benefit for clients from this change and, indeed, TD goes on to say:

However, in the extremely unlikely event of default by us there may be a delay in distributing the funds

I.E. client risk is increased (albeit in unlikely circumstances). I am grateful to my ShareSoc colleague, Cliff Weight, for making the following estimate of the financial gains to TD from this change:

Suppose I have on average £10k cash in my account and they can get 2.01% on 90 day money and 1.51% on 30 day money (I googled these rates for $1m amounts). The difference is 0.5% p.a. =£50 per year.

They should split the benefit 50/50 with investors in my view.

If they have 100,000 customers, this little ploy will net them £5million extra profits a year.

So extra risk for TD’s clients, with no benefit, and a nice financial reward for TD. I find this completely unacceptable and will be writing in the strongest possible terms to TD and to the FCA, on my own behalf and on behalf of ShareSoc’s members.

Please let us have your views by commenting on this post. I will be happy to pass those views on.

Mark Bentley

Mark, You make a number of good points. It is good that you are working on this on behalf of retail investors.

The FCA Final Report on the Asset Management industry points out that price competition in the retail industry is poor. This is another example of it.

I think brokers have been pushing for this change because they used to make a lot of money from the interest they obtained on client cash deposits (which was always a lot less than they paid to clients, which now is mostly zero). This has undermined the profitability of many stockbrokers (aka. platform operators). It was also the case that they used to be able to get higher interest rates by depositing with lower quality banks and deposit takers but not only are clients now put off by that but I think the regulations might have tightened to prevent that.

Thanks Roger… so this is another example of “hidden fees”. Rather than explicitly charging a commission rate that reflects their costs/profits, they would rather quote a more competitive-appearing rate and instead use crafty back-door methods to boost profits which may increase client risk. As Cliff says, this is anti-competitive and non-transparent (cf complex, confusing tariffs from utility providers). Good ammo for my missive to the FCA!

Just got a similar letter from AJ Bell YouInvest

Thanks Mike,

Have received the response below from II/TD. Looks like this is a wider issue. Will post separately on it with ShareSoc’s views on the general issue and action we propose to take, on behalf of investors, in due course.

“Interactive Investor’s primary responsibility is the security of a client’s data, cash and assets. Current FCA rules state that client money must not be placed out on unbreakable deposits of more than 30 days. Due to the capital impact of accepting CASS deposits of 30 days or fewer, a number of banks have stopped accepting client cash altogether. This in turn has meant that investment platforms have been facing difficulties in maintaining the necessary diversification of client money as per their agreed treasury policies. The FCA has recognised the problem, is reviewing the rules and in the meantime has invited platforms to apply for waivers to the 30 day rule as an interim solution. Interactive Investor has applied for this waiver in order to ensure that our strict treasury requirements – which have the express purpose of maintaining robust security for our clients’ cash – continue to be met.

The waiver is not intended to increase interest income for the investment platforms but to ensure that investment platforms are able to keep deposited client funds diversified and secure. Hargreaves Lansdown, Share Centre and other investment platforms have also applied for and been granted the right to place their client money on deposit for 95 days.

We are not in a position to benefit from the rates stated in the ShareSoc report due to our classification as a financial institution.”

Mark Bentley